BLHK - blueharbor bank

High-performing + high-growth bank at potentially cheap valuation

Introduction

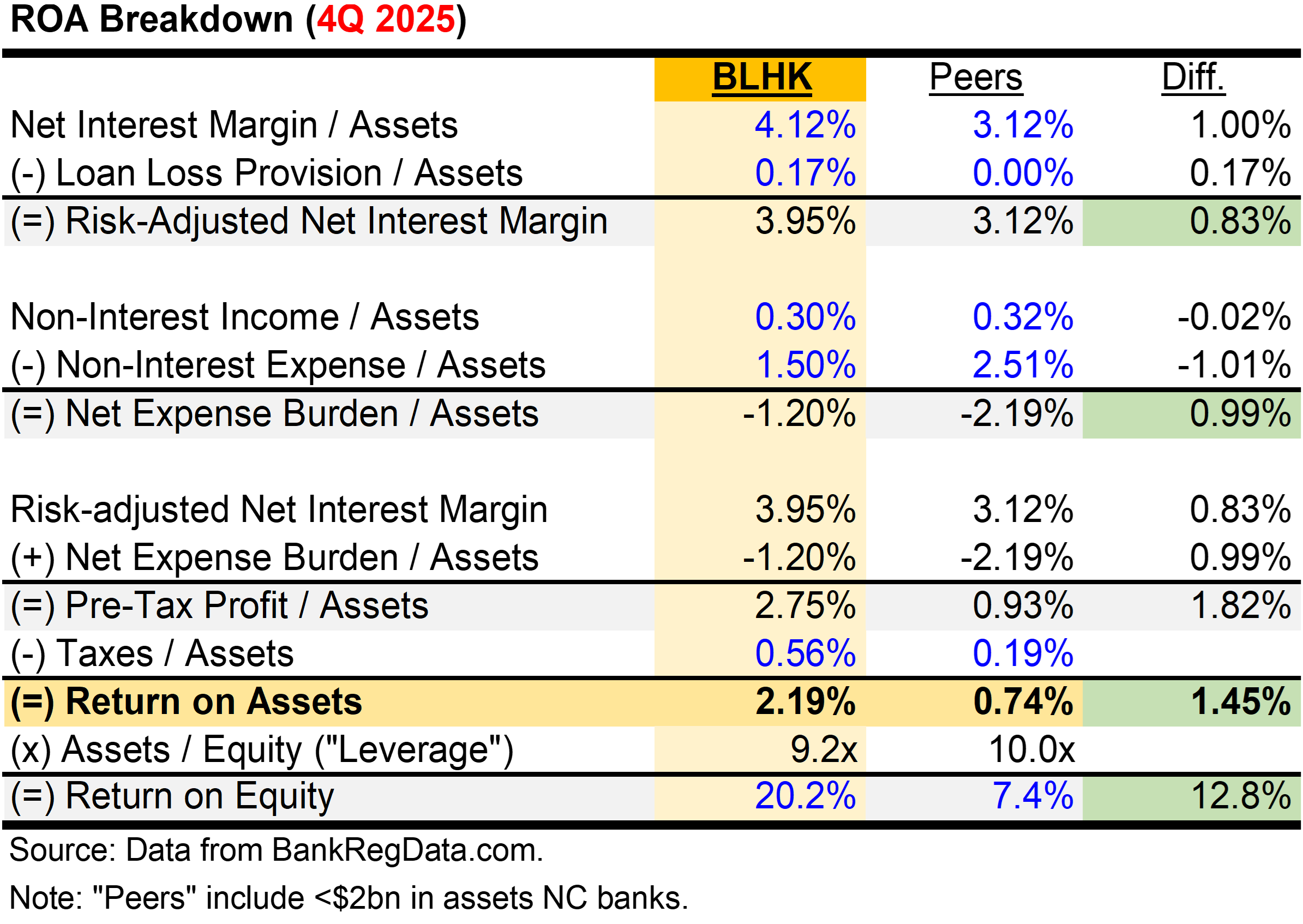

blueharbor bank (OTCQX: BLHK) is a ~$600mm asset bank located in North Carolina. BLHK runs an attractive business model driven by three main factors: (1) high returns on assets driven by structural cost efficiencies and a loan-heavy balance sheet, (2) low historical loan losses and meaningful loss-absorption capacity, and (3) a long record of strong deposit growth.

BLHK currently trades at ~8x forward earnings (based on my estimates) and could achieve a 20%+ five-year IRR under reasonable assumptions (see valuation section). BLHK’s stock is very illiquid and trades on the OTC at a ~$116mm market capitalization, which is likely why the opportunity exists.

High Return on Assets

(1) High Cost Efficiency

BLHK is similar to other banks I have written about previously: its high return on assets is driven in large part by cost efficiency. Also similarly, those efficiencies appear to be structural, stemming from a small three branch footprint paired with a relatively large deposit base (i.e., lots of deposits per branch). Here is a simple example:

Take “Bank A”, with one branch and $100 million of deposits, and “Bank B”, with two branches and the same $100 million of deposits. Both banks have the same deposit base, but Bank B requires an extra branch to support/generate those deposits. That additional branch creates extra occupancy (rent, maintenance, etc.) and personnel expense. As a result, even if everything else about the bank’s are identical, Bank B will produce less profits due to its higher cost structure.

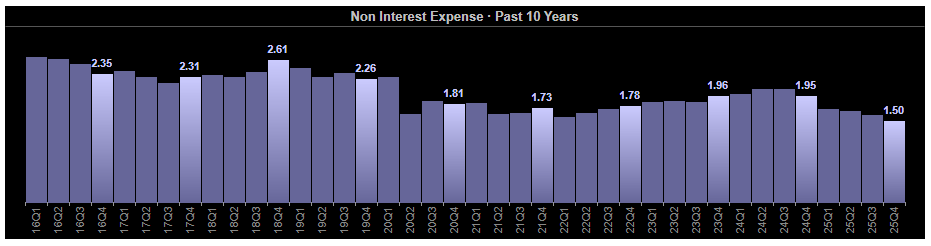

One of the best measures of cost efficiency is noninterest expense as a percentage of assets (“NIE/assets”), shown in the chart below. As BLHK has steadily grown deposits over the past decade, its NIE/assets ratio has declined. Again, simply the effect of meaningfully more deposits generated in the same limited branch footprint. Compared with nearby peers, North Carolina banks with less than $2 billion in assets, BLHK ranks #1 on this metric. It is possible that this ratio continues to improve over time, though possibly not at the same pace seen historically.

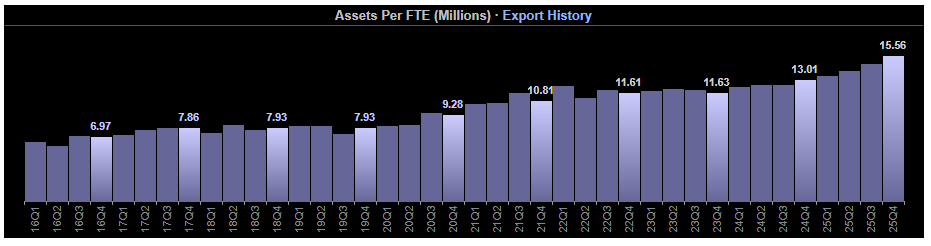

Another useful way to see this operating efficiency is through assets per full-time employee (FTE). BLHK also ranks #1 on this measure, reinforcing that incremental growth was achieved organically rather than via rapid branch expansion and thus a meaningfully larger employee base.

(2) Loan-heavy Asset Mix Drives High Net Interest Margin

The other driver of BLHK’s high return on assets is an elevated net interest margin. To oversimplify, net interest margin is just the difference/spread between the yield the bank generates on its assets and the cost to fund those assets (mainly via deposits).

BLHK’s loan yields are not much higher than the peer median but they do rank #1 in terms of the amount of loans the bank has in relation to assets (i.e., loans/assets). With loans typically yielding higher than securities/cash (a bank’s alternative investments), BLHK’s overall asset yield becomes elevated due to this heavier loan mix. A high yield on assets combined with a relatively average funding cost on their liabilities (again, mainly via deposits) produces the high net interest margin.

Note that for most/many banks an overly heavy concentration of loans could be concerning. More loans typically mean more risk, at least relative to the securities or cash. But, as I mention in the next section, BLHK seems to run their bank in a very low risk manner.

Low Risk - Combination of Low Loan Losses / High Ability to Absorb Losses

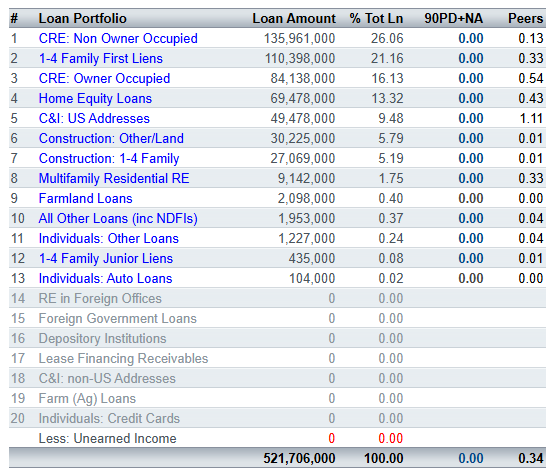

BLHK is a fairly typical community bank with a real estate focused loan portfolio. BLHK is mainly a commercial real estate lender (both investor owned and owner-occupied) and 1-4 family mortgage / home equity lender. They have a self-professed “common sense approach to banking” - which definitely seems to be working.

BLHK’s low risk shines through simply due to having no delinquent loans, ranking #1 among North Carolina peers, with the lowest delinquent loan ratio.

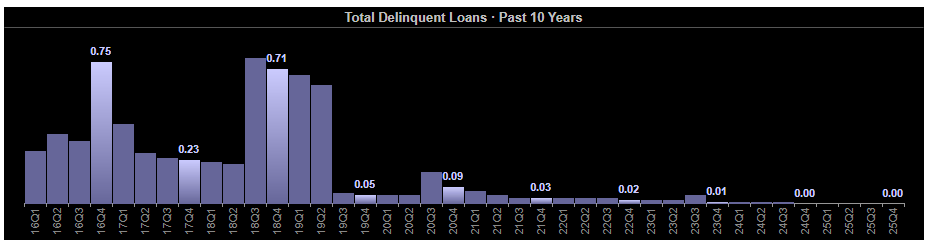

The past ten years have been a similar story with very low delinquent loans with this ultra low (<0.1%) delinquent loan reality beginning in 2019.

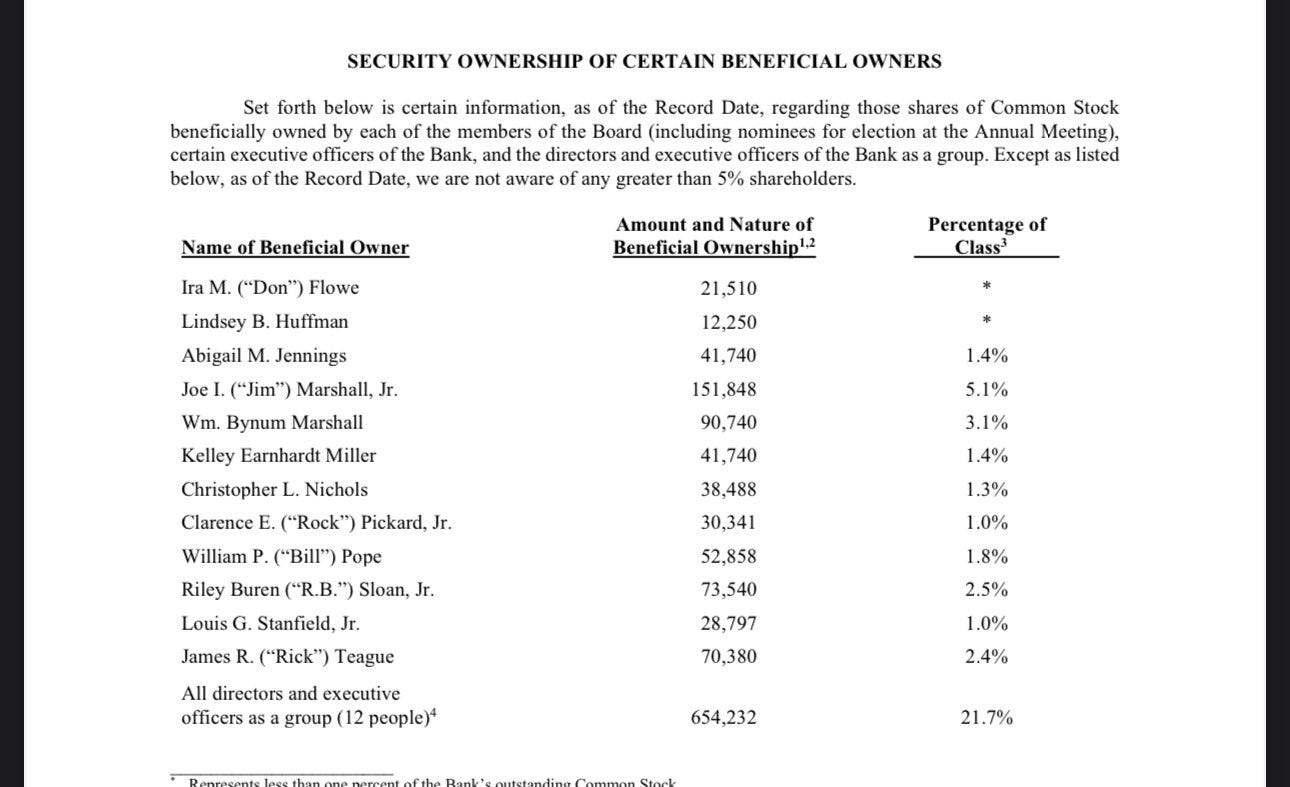

Of course it helps when the bank’s officers and directors own ~22% of the bank, with the CEO owning 5% - alignment of interests with shareholders most definitely exists.

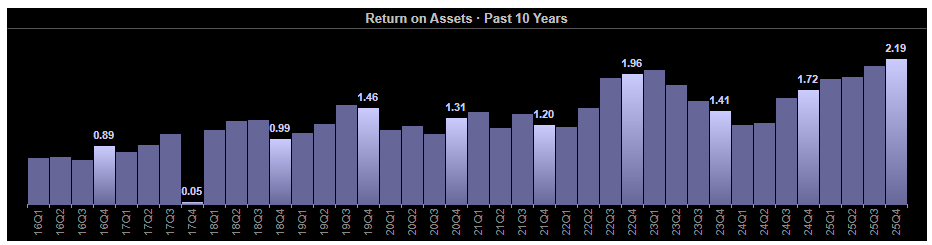

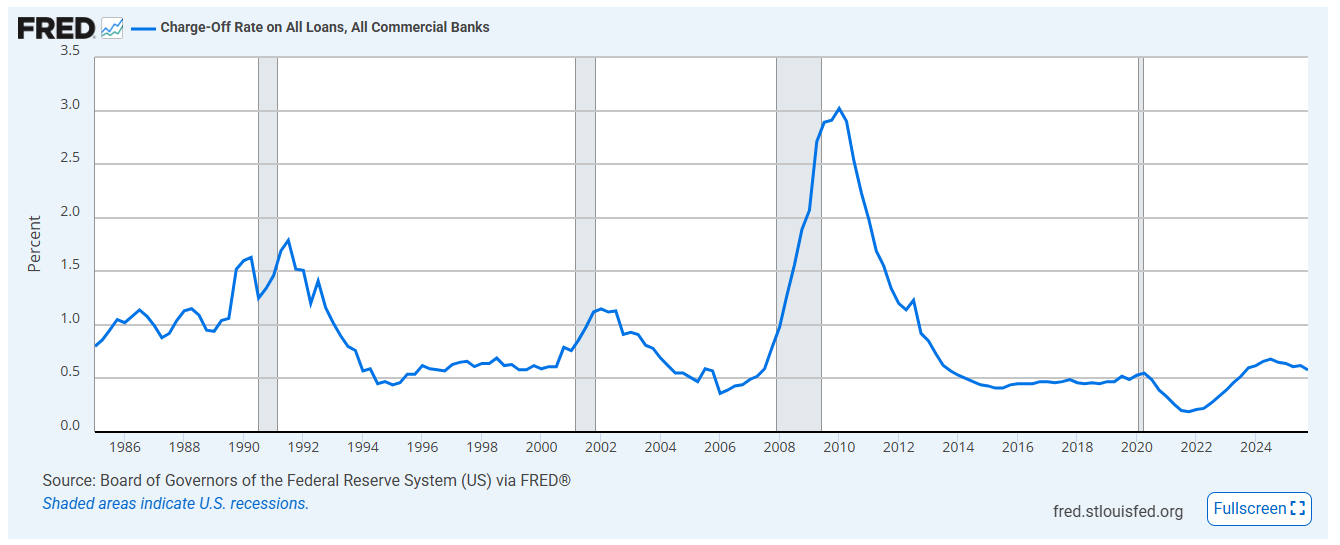

Despite loan delinquencies/losses being non-existent for BLHK, the other factor to consider is their ability to absorb potential loan losses. BLHK currently generates ~17mm of pre-tax, pre-provision income (“PTPP income”) that could offset potential losses. In a hypothetical example, where BLHK incurred losses equal to 3.0%/year on their loan portfolio - the highest quarterly loss rate for all U.S. commercial banks during the 2008-2009 Financial Crisis (see chart below) - they would generate ~$15.5mm of loan losses. With PTPP income of ~$17mm, BLHK would still be slightly profitable for that year.

And, since BLHK has much lower historical and current loan delinquencies/losses, with a well-diversified loan portfolio, it is very likely even under such an adverse scenario, they would perform much better than the average bank did during 2008-2009. Of course, every recession is different but this simple stress analysis gives even more comfort in the bank’s seeming low risk nature.

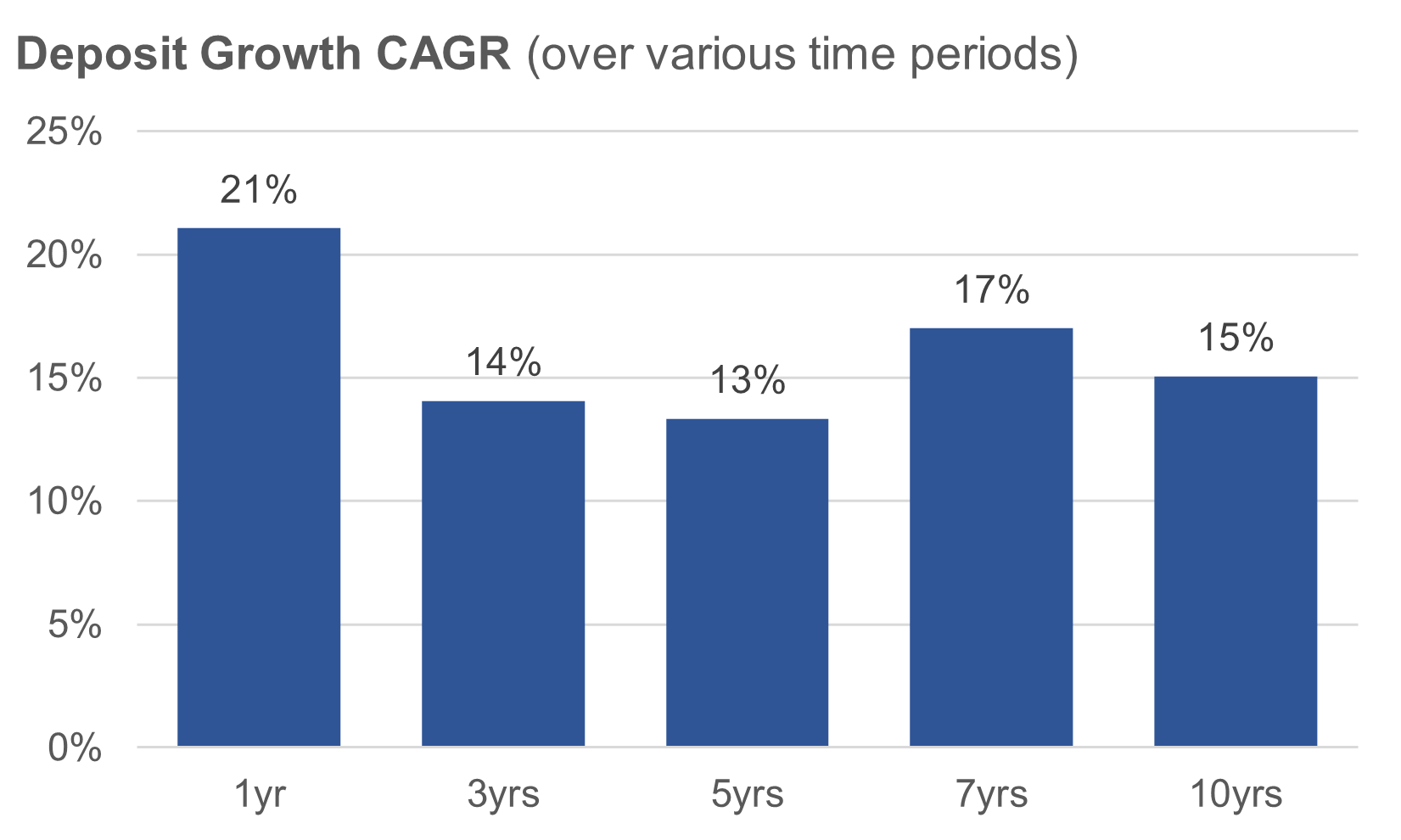

High Deposit Growth

BLHK’s superior profitability and low risk create durable earnings but the ability to generate deposits has helped fuel the bank’s rapid growth. For example, over the past 10 years, the bank has grown deposits at a 15% annualized rate (see chart below). Looking over various time shorter term time periods and this high deposit growth has been relatively consistent.

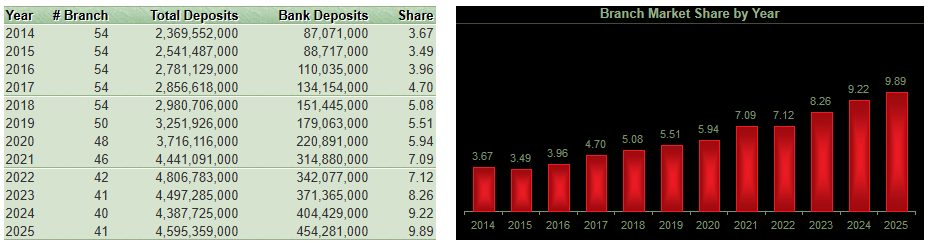

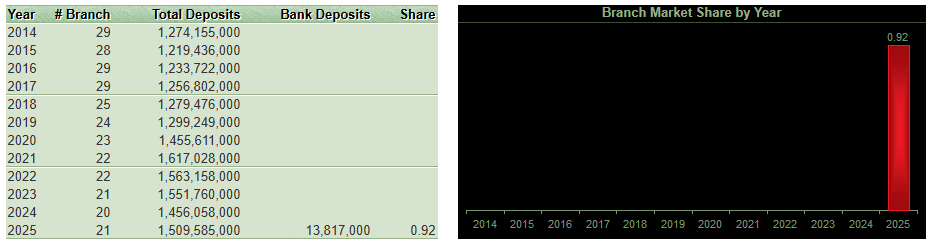

Below is deposit data for the two counties where BLHK operates. BLHK has two branches their main market of Iredell County, North Carolina via their Mooresville and Statesville branches. BLHK has consistently gained deposit market share here over the past ~10 years.

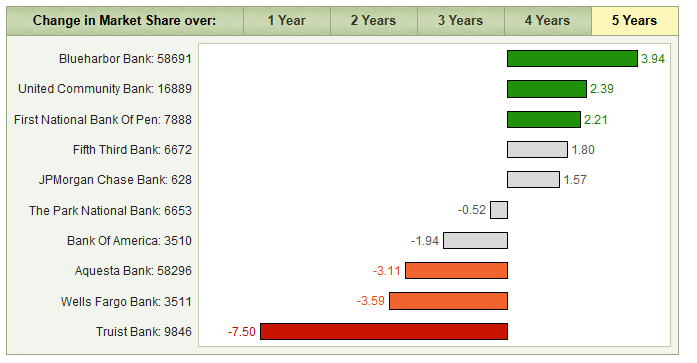

Two more item to note on BLHK’s Iredell County presence, first, they gained the most deposit market share over the past 5 years versus all competitors in the market. This is despite operating in Iredell since the bank’s inception - no new entry “bonus” for BLHK.

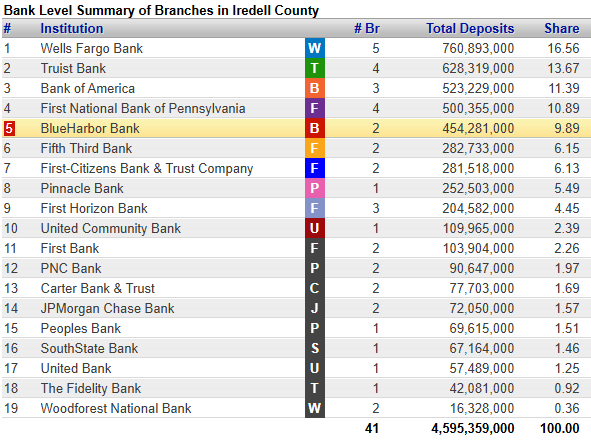

Second, BLHK still has much room to grow and continue to gain share in Iredell County. BLHK only ranks #5 in that market in terms of deposit market share, with the leader - Wells Fargo - at 16.5% share (versus 9.9% for BLHK).

Also, in September 2024, BLHK opened a new branch in the city of Mount Airy - marking their entry into Surry County.

Valuation

Valuing a bank can be simplified down to four main variables: (1) how much will assets grow, (2) what will be the return generated on those assets, and (3) how much of those profits will be excess capital available for distribution to shareholders versus required for growth, and (4) what multiple those future earnings will be valued at.

Asset Growth

Deposits fuel asset growth and, as discussed above, BLHK has consistently generated large amounts of deposits. On the deposit growth chart in the previous section, the lowest annualized growth rate was 13%/year, which was over the last 5 years.

Most banks will grow at local nominal GDP (real GDP growth + inflation rate) +/- if they are taking/losing deposit share +/- growth from new branches in new areas.

Specific to BLHK, they should continue to steal deposit share in Iredell County and gain some additional growth via their new Mount Airy branch.

Return on Average Assets

At the introduction of this article, I showed a breakdown of BLHK’s current return on assets. One could argue that a certain component is a bit high or low compared to what they might do in a “normalized” future year. But, without overcomplicating, I think those nit-picking adjustments largely offset and five years out, the current ~2.2% return on assets is a reasonable (and likely slightly conservative) estimate.

For those curious about what the “nit-picks” are: (1) current Net Interest Margin / Assets might be slightly high but, (2) Noninterest Expense / Assets is likely to continue to fall over the next five years as deposits continue to build-up within their existing branch footprint. The two small adjustments likely net-out in the future resulting in roughly the same ~2.2% return on assets.

Excess Capital

Historically, BLHK has run the bank with a decent amount of excess capital. Their bank currently has an 11.6% leverage ratio, where nationally you might see that figure in the 9-10% range. But it is likely they remain at least somewhat overcapitalized going forward.

Year 5 P/E Multiple

Most well-operated banks can trade at a 12x+ forward earnings multiple in a decent banking environment. Of course, BLHK is OTC-traded and relatively illiquid. As they continue to grow, some of that illiquidity could go away. But with BLHK’s strength and growth profile, trading at 12x earnings seems reasonable as a likely $1bn in assets bank - five years from now.

Given all the above, below are simple projections using those four variables under a “base case”, “high case”, and “low case” and the resulting five-year IRR. The point of the below tables is not precision - the tables exist to roughly estimate different scenarios of future value and potential returns for BLHK.

At current trading prices, BLHK seems like a fairly low risk bank combined with the potential for high future returns.

Other Factors to Consider

Special Dividends + Buyback

BLHK has conducted a few special dividends of increasing size since 2024. The latest announced in February 2026 was for $1.00/share.

BLHK has also conducted share repurchases over the past few years. Although, likely given the illiquid nature of their stock, the bank has been able to buy a limited amount. This is likely why they began to do the special dividends recently.

Disclosure: I/we currently hold shares of BLHK. I/we may buy more or sell shares at any time. Please do your own due diligence before making any investment. None of my posts are investment advice. For full disclaimer, please click here. Feel free to contact me - I can be reached on this site or via my firm’s website here.